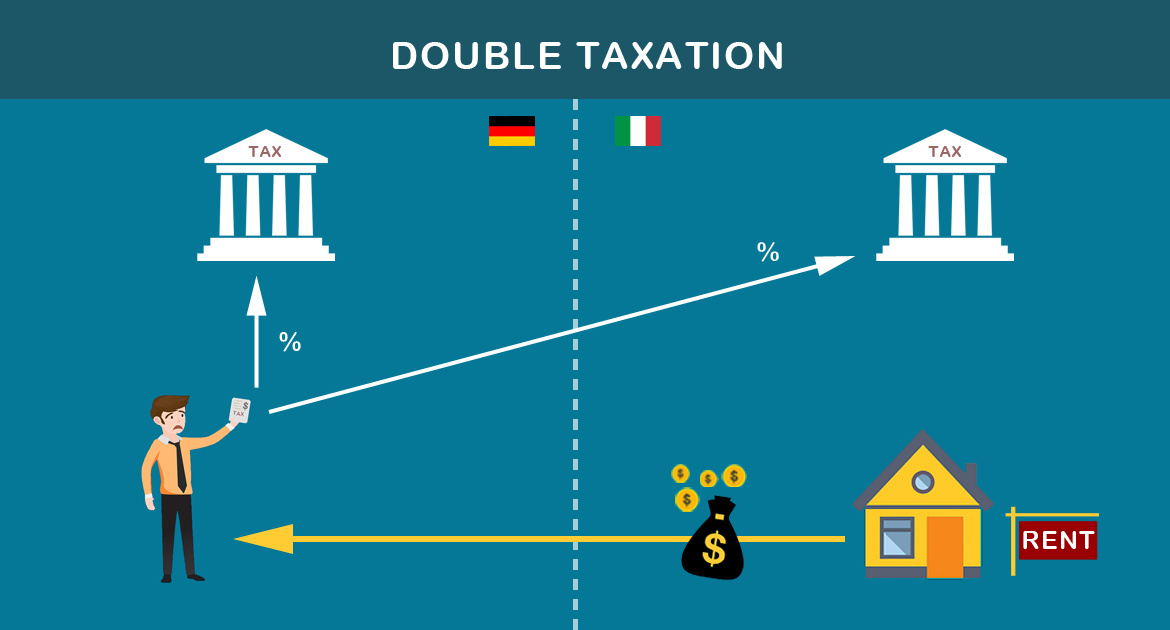

I am German and resident in Germany. I rent my house in Italy on a weekly basis.

How is the rental income taxed in Italy? Is the income also taxed in my country of residence?

Your rental income from managing a property abroad “ausländische Einkünfte” may be taxed both in your country of residence (Germany) and in the country where it is located (in our case, Italy). The country to which income can be derived is called the “source country”.

In general, if you have income from abroad that is not exempt from taxation in your country of residence, double taxation can be avoided (in whole or in part) by requesting a credit for the amount of tax you have paid abroad (source state) or an exemption from taxable base.

This article aims to simplify, and thus make it understandable, the aspect of double taxation.

In the present case, we are assessing a rental income from Italy that is also taxable in Germany.

Initially, it is necessary to take into account that as a resident of Germany you are considered to be subject to unlimited tax liability there (unbeschränkt einkommensteuerpflichtig). Therefore, you also pay taxes in Germany on all your income from abroad (in our case from Italy). In addition, under Italian tax law, rental income is taxable in Italy because the property is located there.

This situation leads to a risk of double taxation (Doppelbesteuerung) if a credit or exemption method is not applied to the foreign derived income.

NOTE:

In Italy you can choose either to pay income tax starting from a rate of 23% or pay an alternative flat tax of 21% called “cedolare secca”. More details in this article: Guide to short term rentals regulations in Italy >>

The “foreign” tax credit method (Anrechnungsmethode), or alternatively exemption method (Freistellungsmethode), is in fact used to prevent double taxation on income derived abroad. It depends on double taxation treaties entered into between your country of residence and the source country. However, we recommend that you contact your accountant or your local Tax Office in Germany in order to accurately assess any tax reliefs currently in force.

It should be noted that a double taxation agreement exists between Italy and Germany in order to avoid the same income being taxed in both countries.

The full text of the agreement can be viewed at this link ==>

Double taxation agreement exists between Italy and Germany

Article 6, first and third paragraphs, of the Double Taxation Convention between Germany and Italy actually provides that “income … from immovable property … situated in the other Contracting State may be taxed in that other State” and such provisions apply to income ” derived from the direct use, letting, or use in any other form of immovable property“.

With reference to a resident of the Federal Republic of Germany, article 24(3) of the aforementioned Double Taxation Convention, which refers to the “Elimination of double taxation“, provides that “shall be excluded from the base upon which German tax is imposed any item of income from sources within the Italian Republic. The Federal Republic of Germany, however, retains the right to take into account in the determination of its rate of tax the items of income and capital so excluded“.

In relation to the present case, a landlord resident in Germany who has received foreign income from renting out his house in Italy can therefore request that the rental income derived from Italy be exempt from the German taxable base. However, the Federal Republic of Germany has the right to take into account that “exempted” income on the determination of the tax bracket.

Let us explain it trough a practical example:

assume that the worldwide income of a resident in Germany amounts to EUR 120,000, of which EUR 80,000 is derived from Germany and the remaining EUR 40.000 represents the rental income from Italy.

1) The Italian tax rate on rental income is a flat tax on 21%.

40,000 x 21 % = EUR 8,400

NOTE! The foreign landlord can choose to pay an alternative flat tax of 21% on rental income according to Italian tax law. This choice should be made directly when drawing up the Italian income tax return or when registering the contract with the Italian tax office.

2) Under the Germany-Italy Double Taxation Convention, Germany applies the “exemption with progression method” towards the income derived in Italy.

In order to simplify the calculation, we don’t take into consideration the real German income tax brackets.

We assume that in Germany the rate of tax on income from EUR 60,000 up to EUR 100.000 is 40%, and on income above EUR 100,000 45%.

As the worldwide income of the residence taxpayer amounts to EUR 120.000, the tax rate applicable would be 45%. However, due to application of the convention, the tax rate (45%) will only be applicable to the income derived in Germany (i.e. resident country). This means that the tax due in Germany will be 80,000 x 45% = EUR 36,000.

In summary:

=> tax levied by Italy => 8,400 EUR;

=> tax levied by Germany => 36,000 EUR.

You claim relief for the Italian tax in your income tax return with reference to the year you report that income from Italy.

* * *

NOTE:

Particular attention should be paid to the submission of the income declaration to the Italian Tax Authority “Agenzia delle Entrate”.

An income tax return for the rental income received must be submitted in Italy each year, even though the landlord is resident abroad (in our case, Germany). Forgetting to submit the declaration in Italy can have serious consequences (high fines) depending on the length of the delay.

Our law firm very often faces problems related to double taxation of income abroad as well as forgetfulness (or delay) in filing the tax return in Italy. This happens more often to people living abroad who receive additional income from renting property in Italy.

If you have forgotten to declare your rental income in Italy, contact an accountant or a lawyer as soon as possible in order to settle your tax position before a tax assessment check is carried out. In this way, the situation can be regulated through the payment of minor penalties/fines.

If you need information regarding the taxation of your rental income from Italy, please contact us. We are happy to provide information and answer all your questions. In addition to this, in the event that legal assistance should be required, our law firm offers a complete customized assistance to foreign landlord who owns a property in Italy by addressing all tax matters even related to double taxation issues.